[ad_1]

Kimberly Draxler was in shock when she known as her mortgage lender in April and was instructed her four-bedroom house in Hillview, Kentucky, can be bought out from below her in a matter of days.

Although she had been alerted that one thing may be mistaken by a letter within the mail from an lawyer providing help in fending off foreclosures, she mentioned her lender by no means knowledgeable her that she was about to lose her house.

“They by no means known as me and instructed me they had been simply going to tear my home proper beneath me,” Draxler instructed CBS Information.

Draxler’s lender mentioned it notifies all debtors of a potential foreclosures by mail and by cellphone all through the method, in compliance with federal debt assortment guidelines.

Earlier than studying that her house was coming into foreclosures, Draxler, who’s 57 and on incapacity, mentioned she stayed afloat financially by counting on her son, who contributed $600 a month to assist deal with family bills. However after he moved out in 2024, her payments started to pile up, she instructed CBS Information. Draxler quickly fell behind on her mortgage.

The monetary pressures bearing down on Draxler spotlight the struggles of householders nonetheless grappling with the rising value of every thing from housing and groceries to vitality payments and insurance coverage protection. With many households stretched skinny, sudden occasions comparable to job loss, unplanned medical expense and even easy automobile issues could cause folks to fall behind on their mortgages.

“I simply could not do it anymore”

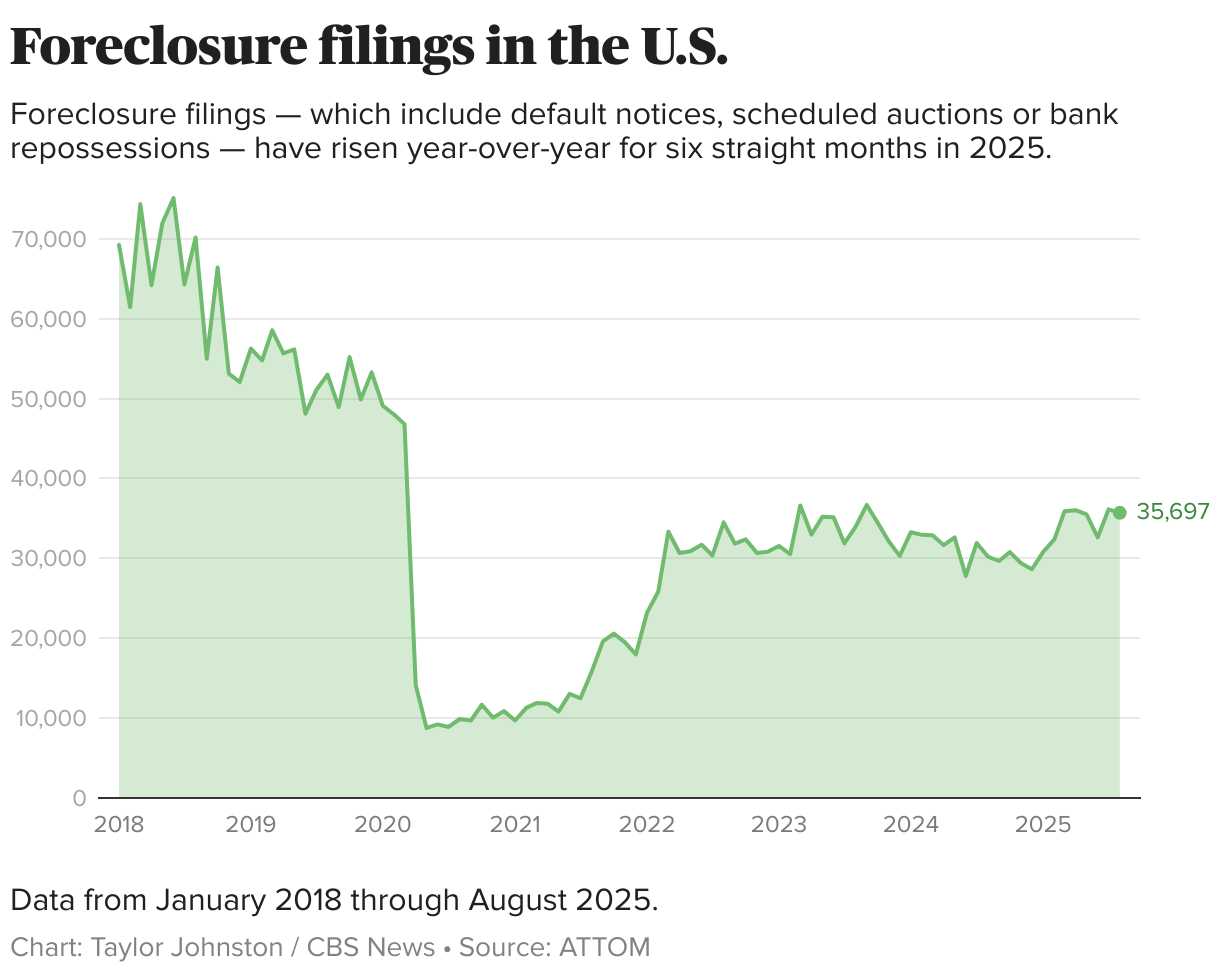

Though foreclosures — which embody default notices, scheduled auctions or financial institution repossessions — stay properly under their pre-pandemic ranges, they’re on the rise.

As of August, foreclosures filings had risen six straights months and had been up 18% from a yr in the past, in keeping with property knowledge agency ATTOM. By June, roughly 188,000 properties had foreclosures filings, placing the U.S. on monitor to surpass the roughly 322,000 U.S. properties that went into foreclosures in 2024.

“Paying for the home, the automobile, the need payments — I simply could not do it anymore,” mentioned Draxler, who had come near dropping her house in foreclosures on three earlier events over the past decade.

Roughly 94% of mortgage defaults happen after a house owner loses earnings to extenuating circumstances, in accordance to The City Institute, citing knowledge from the Nationwide Bureau of Financial Analysis.

Rising homeownership prices

A key issue behind the rise in foreclosures charges is the rising value house insurance coverage, utilities, property taxes, repairs and different homeownership bills. For instance, single-family owners with a mortgage at present pay a median of $2,370 a yr for property protection — up practically 70% from 5 years in the past, in keeping with knowledge from ICE Mortgage Expertise.

Along with rising owners insurance coverage prices, many households are additionally contending with exorbitant property taxes in addition to elevated rates of interest.

“All of those rising prices related to holding a house, you’ve gotten rising strain on present owners to proceed to have the ability to afford and pay for his or her mortgages,” Geoff Smith, government director of the Institute for Housing Research at DePaul College, instructed CBS Information.

Todd Teta, chief product and know-how officer at ATTOM, additionally cited the latest slowdown in hiring as an element behind rising mortgage delinquencies, noting that job loss usually drives foreclosures.

A excessive rate of interest surroundings might be significantly difficult for owners with variable-rate loans, which reset at sure intervals partly primarily based on market situations. Which means a house owner would possibly see a serious bounce of their month-to-month mortgage cost if their reset happens when rates of interest are elevated.

A slim escape

Extra such loans at the moment are hitting their reset intervals, Teta famous, a pattern he expects to proceed. “Whereas there was a small dip in rates of interest, they continue to be considerably increased than just some years in the past, so debtors with upcoming resets are nonetheless prone to see sizable cost will increase.”

As for Draxler, she managed to maintain her house by submitting for Chapter 13 chapter, which permits debtors to carry onto their property and repay debt over time, often inside three to 5 years. However coming so near dropping her house of greater than 30 years continues to weigh on her.

“I didn’t wish to lose my home,” Draxler mentioned. “I would not don’t have any place to go.”

[ad_2]

Hosts Investor Day with Full Agenda")